How to Make a Personal Budget Step by Step (and Actually Stick to It)

If you've searched for how to make a personal budget, you probably already know you should have one. What you're not sure about is where to start, which system to follow, and, above all, how to avoid abandoning it three weeks in — like last time.

This article is not going to tell you to "spend less than you earn." You already know that. What you'll find here is a five-step system you can apply tonight, with real examples, no economics degree required.

Not sure which budgeting method to choose? Here's the summary before you start:

| Method | Difficulty | Monthly time | Best for |

|---|---|---|---|

| 50/30/20 Rule | Low | 10-15 min | Beginners with a fixed salary |

| Kakebo Method | Low-Medium | 20-30 min | Those who want conscious control and lasting habits |

| Zero-based budget | Medium-High | 45-60 min | Detail-oriented profiles or highly variable expenses |

| Envelope method | Low | 10 min | Those who prefer to control spending in cash |

We cover each one throughout the article. If you already know which method you want, you can jump straight to Step 2.

Why 80% of Budgets Fail Before Spring

It is not a lack of willpower. Most budgets fail for the same reason: they are designed to be perfect, not to be real.

The mistake no one tells you: the budget as punishment

When someone decides to "make a budget," they usually frame it as a restriction. Less coffee. Fewer nights out. Less leisure. The result is predictable: you hold on for a few days, an unexpected expense breaks the plan, and since "you've already blown it," you quit.

A budget is not a punishment. It is a map. It tells you where your money goes so you can decide whether that is really what you want.

What makes a budget last

Budgets that work share three characteristics: they are honest (they reflect real life, not ideal life), flexible (they include room for unexpected expenses), and reviewed (someone looks at them every month and adjusts them).

The system you will build in this article has all three.

Before You Start: Understand Your Real Financial Situation

The first step is not writing numbers in a table. It is knowing where you are starting from.

Calculate your real net income (not the gross salary)

Always work with the money that lands in your account, not the gross salary. If you earn €2,200 gross but receive €1,700 net, your budget works with €1,700. Everything above that does not exist for this exercise.

If you have variable income — freelance, commissions, seasonal work — calculate the average of the last six months and use that number as a conservative base.

Fixed expenses, variable expenses, and forgotten expenses: the trio you need to know

There are three types of expenses you need to identify:

- Fixed expenses: The same every month. Rent or mortgage, contracted utilities, insurance, monthly transit pass.

- Variable expenses: They change month to month. Food, leisure, clothing, nights out.

- Forgotten expenses: The ones that don't appear in the monthly statement but happen anyway. Car inspection, dentist visit, birthday gift, annual insurance. These are the ones that destroy budgets that "balanced perfectly."

Calculate your real savings margin before continuing

Enter your net income and expenses to know exactly what number you are working with. It takes 30 seconds.

Calculate my savings margin →

Step 1 — Define How Much Comes In and Goes Out Each Month

This step has one goal: build an honest financial snapshot of the present moment.

How to list all your income

Write down every source of income: net salary, side work, rental income, pensions, benefits. If the budget is shared with your partner, include both incomes. If you have irregular income, include it only if it is recurring and you can estimate it with reasonable accuracy.

How to make an honest inventory of your real expenses

The most effective method is not trying to remember from memory. It is opening last month's bank statement and writing everything down. Without filtering, without judging. Everything that left your account in the last 30 days.

Do not do this exercise to feel bad. Do it to know the truth. The truth is the only valid starting point.

The small-spending trap that never shows up in any bank statement

Small daily expenses are individually small, frequent, and invisible. The morning coffee (€1.50 × 22 working days = €33), the afternoon snack, the subscription you forgot to cancel months ago, the occasional parking fee.

On their own they seem irrelevant. Added up over the month they can represent between €80 and €200 of unplanned spending. We have a specific guide on how to eliminate them using the Japanese method.

Step 2 — Choose the Budgeting Method That Fits You

There is no universal method. There are methods that fit each profile, each level of detail, and each amount of available time.

The 50/30/20 rule: the most well-known method

Divide your net income into three blocks:

- 50% for needs: rent, food, transport, utilities, insurance.

- 30% for wants: leisure, restaurants, travel, non-essential purchases.

- 20% for savings and investment.

It is the simplest method to apply and the most recommended for anyone starting from scratch. Its limitation is that it does not distinguish between types of needs or generate detailed information about your spending habits. But as a starting point, it works.

Calculate your personalized 50/30/20 split

Enter your net income and get the three blocks adjusted to your salary in real time, without any manual calculation.

Calculate my 50/30/20 split →

Zero-based budgeting: total control over every euro

In this method, every euro has an assigned function before the month begins. At the end, income minus all destinations — expenses plus savings — must equal zero. It does not mean spending everything: it means savings are also "assigned" to a concrete goal.

It is the most rigorous method and the one that offers the most control. It also requires the most time upfront. Ideal for detail-oriented profiles or for anyone who already masters the 50/30/20 rule and wants a higher level of precision.

The Kakebo method: budgeting plus awareness

Kakebo is a Japanese household account book that combines three elements: monthly budget + daily expense tracking + conscious review at the end of the month. Unlike the other methods, it does not just organize money: it generates awareness about spending patterns and the habits that drive them.

At the start of the month you define how much comes in and how much you want to save. During the month you record each expense by category. At the end of the month you ask yourself four specific questions that we cover in Step 5.

If you want to understand the complete system, here is the definitive guide to the Kakebo method. And if you want to compare it with digital alternatives like YNAB, here is the Kakebo vs YNAB analysis with their real differences.

Comparison table: which method is yours?

| 50/30/20 Rule | Kakebo | Zero-based | Envelope method | |

|---|---|---|---|---|

| Initial difficulty | Low | Low-Medium | Medium-High | Low |

| Weekly time | 5 min | 5-10 min | 15-20 min | 10 min |

| Level of detail | Low | High | Very high | Medium |

| Variable income | Poor fit | Very adaptable | Adaptable | Poor fit |

| Creates habit change | Little | A lot | A lot | Some |

| Best for | Beginners | Conscious control | Maximum rigor | Cash spending |

Step 3 — Classify Your Expenses with Criteria

Once you have chosen your method, you need to classify your expenses. Kakebo's classification is the most useful because it distinguishes why you spend, not just what you spend on.

Survival expenses: what you cannot eliminate

Everything you cannot cut without affecting your basic life: rent or mortgage, food, home utilities, essential transport, medication, required insurance. This is the most stable block of your budget.

Warning sign: if this block exceeds 60-65% of your net income, you have a structural problem that no savings method can solve without changing a major variable: housing, transport, or income.

Optional expenses: what you choose to spend

Everything you decide to spend: leisure, restaurants, non-essential clothing, entertainment subscriptions, travel, treats. This is the block where you have the most room to adjust without compromising your essential quality of life.

The key is not to eliminate it. It is to decide it consciously. There is a real difference between spending €200 on leisure knowing you are choosing to and spending €200 without knowing exactly how or when it disappeared.

Savings and unexpected expenses: the most ignored category

This block has two components that most people confuse: active savings — money you set aside with a defined goal — and the buffer for unexpected expenses — money for the forgotten expenses we mentioned earlier.

If you do not include a buffer for unexpected expenses in your budget, every unexpected cost will break the plan. Not because you are disorganized, but because the plan was not realistic.

Practical classification table with examples:

| Block | Examples | Rough percentage |

|---|---|---|

| Survival | Rent, food, utilities, transport, insurance, medication | 45–55% |

| Optional expenses | Leisure, restaurants, clothing, subscriptions, travel | 20–30% |

| Active savings | Emergency fund, specific goal | 10–20% |

| Unexpected buffer | Car inspection, dentist, gifts, minor repairs | 5–10% |

Step 4 — Set Your Savings Goal

A budget without a savings goal is just an expense log. The goal is what gives the system purpose.

How much should you save each month based on your situation?

The standard answer is "20% of your income." That figure makes sense as a reference but ignores individual reality. If you live in an expensive city, have a high mortgage, or are getting out of debt, 20% may be unreachable.

A more honest way to answer: save the maximum you can sustain consistently for twelve consecutive months, even if it is 5%. Consistency builds more wealth in the long run than an amount you abandon in March.

If you want to calculate your real savings goal based on your income and expenses, the savings calculator gives you the number in seconds.

The first goal for anyone: the emergency fund

Before saving for a vacation, a car, or any other goal, there is one priority that admits no argument: the emergency fund. It is the money that covers between three and six months of your basic expenses in case of job loss, illness, or any major unexpected event.

Without that cushion, a life setback becomes debt. With it, an unexpected expense is an inconvenience, not a catastrophe.

How to distribute savings across time horizons

Once the emergency fund is covered, distribute savings by time frame:

- Short term (under 1 year): Vacation, appliance, planned treat.

- Medium term (1–5 years): Car, down payment on housing, education.

- Long term (over 5 years): Retirement, financial independence.

You do not need to save for everything at once. Emergency fund first. Then one concrete goal. That way savings have purpose and purpose sustains the habit when motivation wanes.

Step 5 — Review, Adjust, and Don't Give Up

The budget you build in January is not the one you need in October. Life changes. Expenses change. The budget has to change too.

The monthly review: 20 minutes that change your relationship with money

Once a month, with your bank statement in front of you, compare what you planned with what actually happened. Not to punish yourself, but to learn. If the food block consistently exceeds budget, or the leisure block always goes over plan, that is valuable information, not a moral failure.

The monthly review is the most important act in any budget. Without it, the budget is just last month's list of intentions.

The 4 Kakebo questions that every budget should answer

The Kakebo method closes each month with four specific questions that turn numbers into reflection:

- How much money do I have? — Actual income for the month.

- How much money have I spent? — Total actual spending.

- How much money have I saved? — Real difference between income and expenses.

- How could I improve? — Without judgment, just honest observation.

These four questions are what separates the Kakebo method from any spreadsheet. Knowing the numbers is not enough: you need to understand what drives them.

What to do when the budget doesn't balance

If when reviewing the month you see you spent more than planned, do not restart from scratch. Adjust. Move margin from one block to another, identify the specific expense that broke the plan, and decide whether it was a one-off event or a recurring pattern you need to accommodate next month.

A budget that gets adjusted works. A budget that gets abandoned when it doesn't balance perfectly does not.

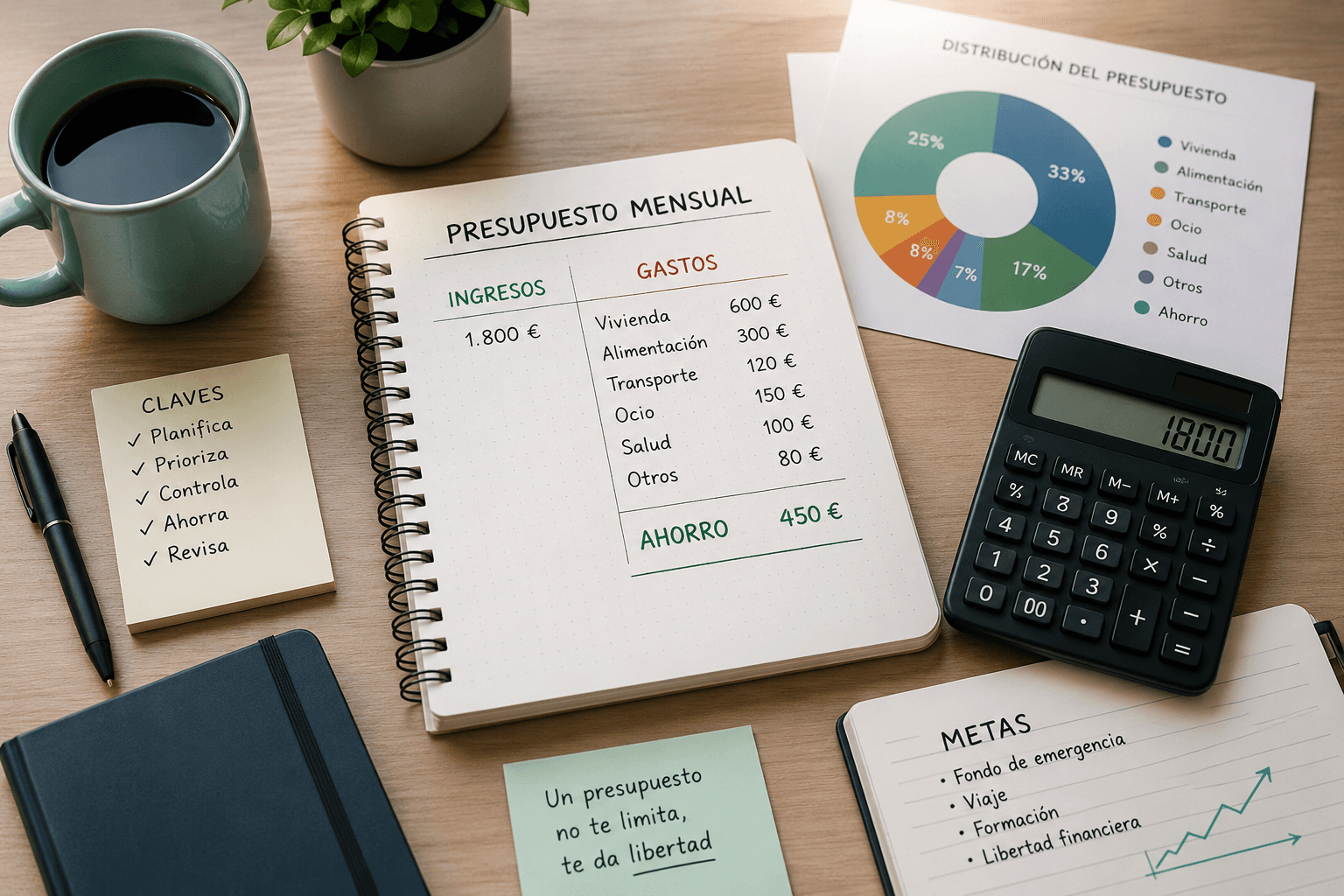

Complete Personal Budget Example — Month by Month

To understand how this looks in practice, here is María's budget: 32 years old, graphic designer, net salary of €1,800 per month, renting in a mid-sized Spanish city.

Starting point:

| Concept | Amount |

|---|---|

| Monthly net income | €1,800 |

Complete distribution:

| Block | Category | Monthly spending |

|---|---|---|

| Survival — 53% | Rent | €650 |

| Food (supermarket + market) | €230 | |

| Utilities (electricity, water, internet) | €110 | |

| Transport (monthly pass + occasional fuel) | €60 | |

| Private health insurance | €42 | |

| Subtotal | €1,092 | |

| Optional expenses — 20% | Leisure and outings | €150 |

| Restaurants and cafés | €80 | |

| Clothing and personal care | €70 | |

| Subscriptions (streaming, apps) | €28 | |

| Miscellaneous optional | €32 | |

| Subtotal | €360 | |

| Active savings — 14% | Emergency fund (goal: €1,350) | €150 |

| Summer trip savings | €100 | |

| Subtotal | €250 | |

| Unexpected buffer — 5% | Unplanned expenses | €98 |

| TOTAL | €1,800 |

With this distribution, María completes her emergency fund in 9 months. The €1,350 goal covers exactly three months of her basic expenses (€450 minimum survival). At the same time, she saves for her trip without eliminating monthly leisure or living at the limit.

The €98 buffer covers real expenses like a medical check-up, an unexpected gift, or a minor home repair. If a month it goes unused, it carries over. If a month it is exceeded, she adjusts leisure for the following week.

This budget is not perfect. But it is honest, sustainable, and adjustable. That is what makes it real.

The 5 Mistakes That Ruin Any Budget (and How to Avoid Them)

Mistake 1: Budgeting too tight

The ideal budget on paper may be impossible in practice. If you eliminate all leisure, all social spending, and all margin for error, the first weekend with friends destroys it. A good budget is not the most austere one: it is the one you can maintain for twelve months in a row.

Mistake 2: Not including annual expenses in the monthly calculation

Car insurance, inspection fees, the dentist, vacation, Christmas gifts. All are real expenses that happen every year but do not appear in the monthly statement. The solution is simple: estimate them, add up the annual total, and divide by twelve. Add that monthly quota as a fixed category in your budget.

Mistake 3: Not comparing what you planned with what actually happened

A budget that is not reviewed at the end of the month is just a wishlist. The comparison between plan and reality is 80% of the value of the system. Without it, the budget becomes a document created in January that is never looked at again.

Mistake 4: Forgetting the buffer for unexpected expenses

Unexpected expenses are not actually unpredictable. Something always happens: a breakdown, a fine, an urgent purchase, a medical visit. A budget without an unexpected buffer turns every surprise cost into an emergency that breaks the plan. Always include a category for it, even if small.

Mistake 5: Quitting when one month doesn't balance

A bad month does not mean the system does not work. It means there is something to adjust. Budgets that last for years are not the ones that never fail: they are the ones that get corrected each time something does not balance. Imperfect consistency produces real results. Abandoned perfection produces nothing.

Frequently Asked Questions About Making a Personal Budget

How long does it take to make a personal budget for the first time?

The first time, between 45 minutes and one hour if you have last month's bank statement to hand. From the second month on, the monthly review and adjustment takes no more than 20-30 minutes.

How much should I save each month?

There is no universal figure. The most cited rule is 20%, but the most important thing is that the amount is sustainable for twelve consecutive months. Use the savings calculator to calculate your real margin.

Is it better to use paper, Excel, or an app?

It depends. Paper — in the Kakebo tradition — generates the most awareness because it forces you to record by hand. Excel gives flexibility but requires building the system yourself. Our guide on the Kakebo Excel template covers the pros and cons. A specialized app combines structure and convenience with the least setup time.

What if my income changes every month?

Calculate the average of the last six months and use that as a conservative base. In higher-income months, the surplus goes to the emergency fund or the current savings goal. We have a specific guide on budgeting with irregular income using the Kakebo method.

What is the difference between budgeting and tracking expenses?

The budget is the plan: you decide in advance where each euro goes before the month starts. Expense tracking is the execution: you record where each euro actually went. Both are necessary. Without a budget, expense tracking is just a diary with no direction. Without expense tracking, the budget is a list of good intentions.

How often should I review my budget?

A monthly review is mandatory and should take no more than 20 minutes. A quick 5-minute weekly check-in is optional but useful for catching deviations before they compound. An annual review is useful for adjusting large categories and updating long-term goals.

Can a budget work on minimum wage?

Yes, though with real structural limitations worth acknowledging. With lower income, the goal is not always to save more but to spend better. Our guide on how to save on minimum wage or as a student addresses this situation directly.

Related Articles

- How to save money every month: 15 proven techniques

- How to eliminate small daily expenses with the Japanese method

- Kakebo vs YNAB: which budgeting method is right for you?

- How to save as a couple without arguing

- The dangers of automatic savings apps and open banking

You have the system. Now you just need a place to use it.

You can start tonight with pen and paper. Or you can use MetodoKakebo: a digital expense journal built on the Japanese method.

No bank connection. No access to your financial data by anyone. No hidden subscriptions. You record your expenses yourself, as they happen, and see exactly where your money goes month after month.

Start your budget today — it's free

Related articles

How to save money every month: 15 proven techniques that actually work

Discover 15 actionable and realistic methods to start saving today, from the 50/30/20 rule to the 52-week challenge.

How to eliminate "gastos hormiga" (Latte Factor): The foolproof Japanese method

Discover what the "latte factor" or small daily expenses are, how the Kakebo method helps you detect them effortlessly, and how much money you could save a year.

Kakebo vs YNAB: Which is the best budgeting method for you?

If you are torn between ancient Japanese simplicity and the strict American zero-based system, here we break down which one best suits your personality.